The most recent study conducted by the Polish Chamber of Insurance* shows that almost 80% of residents of areas particularly exposed to natural forces believe that their dwellings are safe. PIU starts the #niezaklinaj (#dontplead) campaign.

- More than half of the respondents believe that climate changes are causing more and more damage around the world, but not where they live.

- One-third of the respondents believe that insurance against natural disasters is unnecessary due to a low level of risk.

- The studies were conducted only in areas with a particularly high exposure to natural disasters or in regions where a natural force would result in high social or economic costs.

As many as 66% of the respondents think that the probability of flooding in their local area in the next 12 months is low or very low. However, the vast majority of the respondents live in the south of Poland, a region particularly vulnerable to flooding. The respondents’ declarations have an impact on their attitude to insurance. More than 30% of those with household insurance declare that they do not purchase policies covering strong winds. A total of 27% have no protection against voltage surges, which can cause damage to household appliances, radio and TV equipment. One in four respondents decides against flood insurance.

No savings for disasters

As many as 80% of the respondents would not be able to use their own funds to rebuild their damaged property or buy a new one of a similar standard. The situation is the same when it comes to renting new accommodation – for more than 60% of the respondents it would be financially impossible. What is more, a similar number of respondents declare they have no savings they could use if damage is caused by weather events. Therefore, it may seem that most of the respondents would claim household insurance to be the best protection against the effects of natural forces.

Help from the family or the state

However, for damage caused by natural forces, most respondents count on assistance from the local government or the state (54% and 50%, respectively). A total of 52% declare that they would seek help from their family or friends, and almost 50% would immediately notify their insurance company. ‘Despite the growing frequency and severity of weather events, we still take natural forces with a pinch of salt. We are under the impression that damage caused by the elements is more likely to happen to everyone else, but not to us. It is our duty to educate people on insurance; this is why we have launched the #niezaklinaj campaign’, says Rafał Mańkowski, PIU expert analyst. As part of the #niezaklinaj campaign, PIU has conducted studies on awareness about weather risks and insurance. New content has been published on social media and on PIU blogs. In addition, PIU has distributed materials with guidelines on proper protection against severe weather across more than 2400 districts.

Guidance material on the PIU website

Information about the #niezaklinaj (#dontplead) campaign

How can we protect ourselves?

We are unable to avoid natural disasters, but we can mitigate their consequences. Preventive measures, such as spatial planning, or the absence of investment on floodplains, are crucial. Over recent years, the frequency of severe weather events, such as violent storms, heavy rainfall, hailstorms and gales, has increased in Poland. When buying insurance for a house or a flat, we should remember a few simple rules:

- The sum insured should reflect the value of the property we want to protect.

- We should protect not only the walls, but also the items within our property, such as household appliances, radio/TV equipment and furniture.

- The insurance cover should be extensive and include damage caused by rain, flooding, hailstone, gales, fire or lightning.

- We should determine the method of valuation of property in the event of any future damage.

*A study commissioned by the PIU, conducted in July 2019 by SW Research with the use of the CAWI+CATI method on a sample of 2,193 respondents. The respondents were from the provinces of Dolnośląskie, Małopolskie and Podkarpackie, and from the districts of Grudziądz, Inowrocław and Wrocław. According to the PIU report ‘Climate of risk’, these regions are particularly exposed to weather events or are places where extreme weather events could result in significant social and economic costs. Due to the different nature of weather risks, the study did not cover the largest cities of the regions in question, i.e. Wrocław, Rzeszów and Kraków.

The Polish Chamber of Insurance launches an education campaign under the slogan #niezaklinaj (#dontplead). It is aimed at making Poles aware of the increasing risks and consequences of climate change. PIU emphasises that, in order to avoid the consequences of climatic events, appropriate prevention and good insurance are a must.

DOWNLOAD EDUCATIONAL MATERIALS IN PDF

DOWNLOAD EDUCATIONAL MATERIALS IN JPG

– ‘The PIU and Deloitte report “Climate of risk” clearly indicates the growing risks from the effects of climate changes. The educational campaign is essential if we want to be better prepared to face the consequences of climatic events. We want to engage local authorities, insurance agents and the media’, – says Marcin Tarczyński, manager for communication and analyses at PIU.

How aware are we?

The first element of the #niezaklinaj campaign is to study awareness about weather risks and insurance. The respondents were 2,000 residents of provinces with the highest risk of gales, storms and flooding – e.g. the Małopolskie and Podkarpackie provinces. The purpose of the survey is to check the extent to which Poles are aware of weather risks, the sources from which they get information on dangers, what preventive measures they take, and what they would do if they suffered damage. The survey also covers the approach to insurance, especially for houses and flats.

#dontplead, act

The ‘Climate of risk’ report indicates that only 60% of houses and flats in Poland are insured against flooding. . ‘The frequency and intensity of weather risks and natural disasters in Poland are due to rise, which means that both the state budget and the victims will need to pay a higher cost. This year’s heavy rainfall, storms and flooding are the best examples. We should change our “this won’t happen to me” way of thinking and stop casting weather spells. We really can do a great deal to be prepared for the consequences of climate change’ – stressed Marcin Tarczyński.

Learning aids

As part of the #niezaklinaj (#dontplead) campaign, the Polish Chamber of Insurance presents educational videos and graphic materials which show the best way we can prepare ourselves for gales, storms, hailstorms and floods, what to do if we suffer damage, and how to submit insurance claims. It also advises on the inspections that should be done regularly on detached houses and how to ensure their safety and good technical condition. PIU will provide the relevant materials to district offices and insurance agents throughout Poland. ‘We want to encourage local authorities to become actively involved in educating the Polish people. The effects of severe weather events can often be easily contained, by simply moving a vehicle, tidying up the garden or terrace. We would like to convince local governments to display our information materials on the information boards in their districts. We will make the materials in printable formats. The campaign will also involve public relations and promotional activities through our own channels: the nawypadekgdy.pl blog, the PIU expert blog and on social media’, says Agniseszka Durska, communication expert at PIU. Some educational materials are to be created in cooperation with well-known influencers, including Janina Daily, Jarosław Turała, and Aleksandra and Piotr Stanisławski, authors of the popular ‘Crazy Nauka’ blog. They are going to educate the audience on selected weather events, their causes, risks and ways to protect against them.

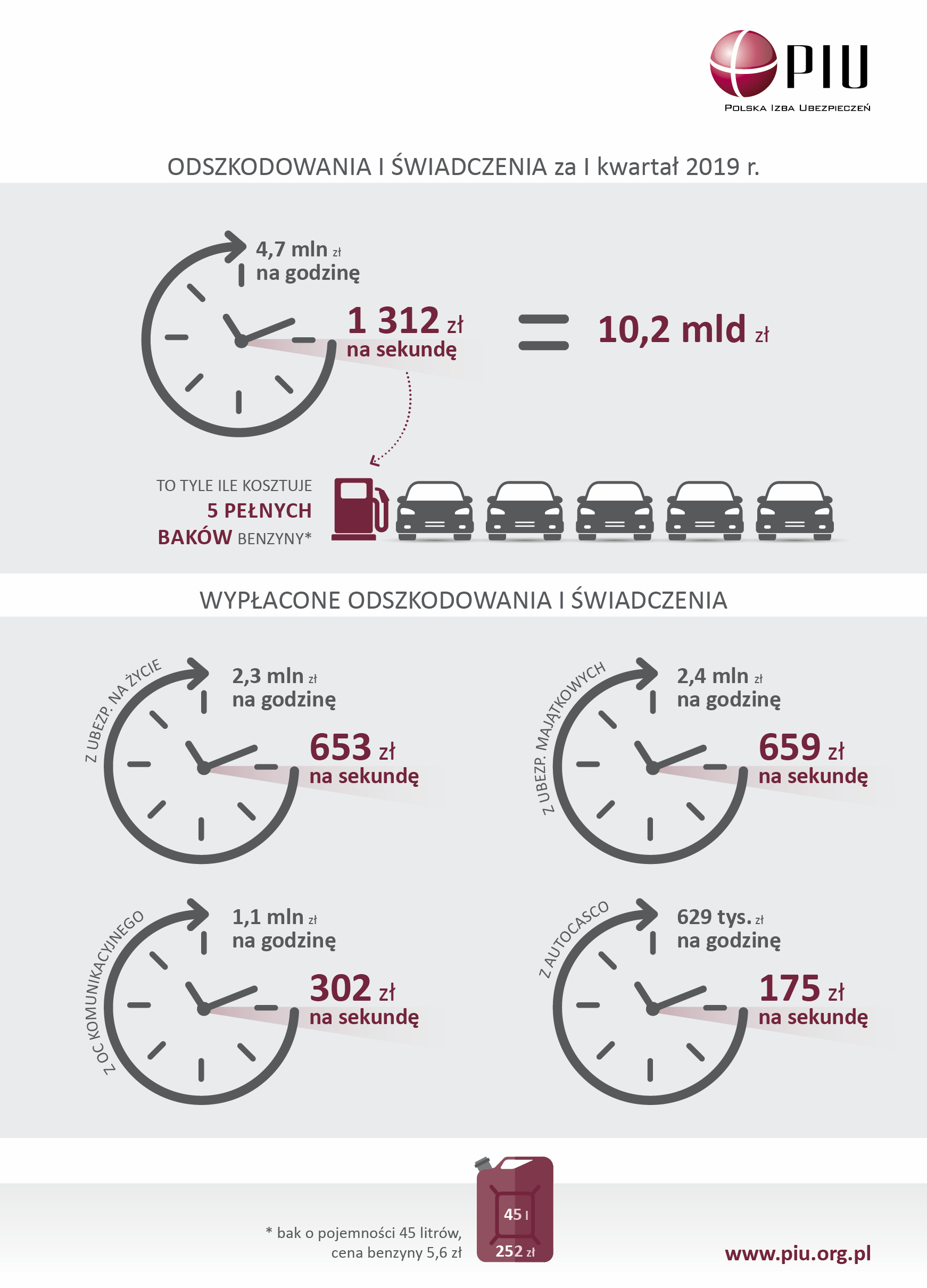

In Q1 2019, Poles received PLN 10.2 billion in insurance compensation and benefits. Each hour of an insurer’s work amounted to PLN 5 million in aid for the injured. In Poland, damage covered by RCA is repaired once every thirty seconds.

Key insurance market figures after Q1 2019

- PLN 10.2 billion for the injured, including:

- PLN 5.1 billion for life insurance

- PLN 3.7 billion for motor insurance

- PLN 1.4 billion for other insurance

- Insurers invested PLN 74.6 billion in assets in domestic bonds and other fixed-income securities supporting the economy and public finance

- PLN 16.8 billion in assets invested in shares of WSE companies and other variable-income securities

- PLN 343 million of income tax will be paid by insurers to the State budget

‘In the first quarter of this year alone, insurers compensated more than 300,000 damages covered by RCA. The injured received more than PLN 2.3 billion in compensation and benefits, which is more than 2.5% more than the previous year’, said J. Grzegorz Prądzyński, president of the Board of the Polish Chamber of Insurance.

Insurers ready for sudden weather phenomena

In Q1 2019, Poles spent almost PLN 6 billion on the protection of their vehicles, of which approx. PLN 3.7 billion constituted RCA contributions and approx. PLN 2.2 billion were comprehensive cover contributions. At the same time, we bought insurance against the effects of natural forces for more than PLN 1 billion. ‘The results for Q1 do not cover the costs of the flooding and windstorms which occurred in May this year. However, it is known that insurance companies are prepared for all weather conditions, both in organisational and financial terms. The simplest damages are already liquidated within one day and insurers commonly use simplified liquidation procedures’, explained Andrzej Maciążek, vice-president of the Board of PIU.

State budget support

Poles spent more than PLN 5.2 billion in Q1 2019 on life insurance, which is 7.7% less than

in the same period last year. They received almost PLN 5.1 billion in benefits as a result.

‘Popularisation of individual protection of life and health is one of the biggest challenges in the insurance market. We live longer and our standard of living is increasingly higher; we often have credit liabilities for several decades. Proper life insurance should be the standard in terms of protecting our closest family’, stressed J. Grzegorz Prądzyński.

In Q1 2019, Polish insurers produced more than PLN 1.1 billion of net profit — 8.6% more than in the previous year. This means PLN 343 million of income tax for the State budget. In addition, insurance companies also paid approx. PLN 120–130 million of so-called asset tax.

You are invited to read the report by the Polish Chamber of Insurance, describing the bancassurance market in Poland after Q1 2019. The premium obtained in the bancassurance channel amounted to PLN 1.2 billion in Section 1 and 580 million in Section 2..

Report

The global market for new mobility in 2030 will be worth 4.3 trillion dollars, according to the analyses by McKinsey & Company. The popularity of new means of transport is growing thanks to development of technology, urbanisation and green attitudes. The Polish Chamber of Insurance (PIU) has developed a report on personal transporters, describing their characteristics, legal status and impact on insurance.

Download the report >>> New urban mobility. What does it mean for insurance?

According to UN data, the population in cities will grow by almost 10% by 2025[1]. More and more people will be looking for ways of moving around the city efficiently.

‘In addition, increasing environmental awareness leads us to give up on cars, at least from time to time. A declaration like that has been made by 79% of Poles in the Eurobarometer survey, carried out in 2017’, said Łukasz Kulisiewicz, a PIU expert.

The new face of urban mobility

The international Light Electric Vehicle Association (LEVA) defines personal transporters as two/three-wheel motor, fuel cell or hybrid vehicles, weighing up to 100 kg. They include electric bicycles and scooters, as well as Segways and hoverboards. The popularisation of personal transporters has been greatly influenced by the development of lithium-ion batteries and co-sharing economics.

Around 10 years ago, the first urban bicycle programmes appeared. Personal transporters are the most recent wave of urban mobility. Their enormous advantage is the possibility of leaving the vehicle at any point where we end a journey and efficiency over short distances. This means that we can quickly cross the so-called ‘last kilometre’, i.e. the section to the target location, e.g. a city transport station.

We need insurance coverage….

According to EU Directive 168/2013, personal transporters are vehicles with a top speed of 25 km/h and a power of up to 250 W. They are not subject to approval. Therefore, they are not covered by the obligation to have to have registration plates and their users do not need to have a driving licence or RCA insurance. Moreover, there are no uniform regulations which define what traffic rules should be applied to personal transporters. This translates into a lack of adequate insurance coverage. Rental company regulations generally pass on the liability arising from accidents to users.

… and regulations

The condition for the existence of personal transporters is ensuring the safety of all road traffic participants and appropriate legal regulations, taking into account the large number of new types of mobile vehicles.

‘The challenge is to amend the Traffic Law. The areas where such vehicles can be operated and their speed limit must be defined. In Barcelona, personal transporters were divided into three classes and their dimensions, safety, insurance and minimum age requirements were defined.

However, in the Netherlands, none of the electric scooter rental companies has been granted authorisation to operate them so far. In the UK, personal transporters can only be operated on private premises’, said Łukasz Kulisiewicz, a PIU expert.

It is worth noting that personal transporter users are exposed to more frequent accidents, for example in comparison to cyclists. This represents an opportunity to create new insurance products.

[1] Population Division of the UN Department of Economic and Social Affairs, 2018 Revision of World Urbanisation Prospects

In 2018, insurers paid out nearly PLN 42 billion to customers and the injured. The value of the assets of insurance companies exceeded PLN 192 billion. In Poland, our protection is ensured on a daily basis by several thousand insurance agents and more than 200 people conducting agency activity.

More data on insurance in Poland can be found in the annual publication of PIU entitled ‘Insurance Figures’. Enjoy the read!

We would like to invite you to participate in the 7th Polish Chamber of Insurance Congress ‘Europe — innovations, inspirations, regulations’, which will be held on 8 and 9 May 2019 at the Sheraton Hotel in Sopot. You can register online at http://kongres-piu.pl/

At total of 2.6 million Poles were using private health insurance at the end of 2018, according

to data from the Polish Chamber of Insurance — over 23% more than the previous year. This number has exceeded 2.5 million for the first time in history, and interest is continuing to grow. We spent PLN 821.1 million on private health insurance in 2018 compared to PLN 678.9 million last year.

‘According to our research, Poles choose to rely on private medical care in particular because of faster access to doctors. It is not surprising because the waiting time for guaranteed health benefits has been steadily increasing for more than two years. At the end of 2018 and 2019, it amounted to 3.8 months’, commented Dorota M. Fal, advisor to the Board of the Polish Chamber of Insurance. ‘We expect effective and quick medical assistance from private medical facilities. This is important for many people, especially in the light of recent media reports about the situation in public healthcare. Private insurance guarantees help when health problems arise. What is important is that it is much cheaper than paying out of pocket for each visit to doctors or expensive tests’, added Dorota M. Fal.

Cooperation with employers is key to better healthcare

The high level of interest of Poles in private healthcare was also confirmed by the study ‘Co-financing healthcare’, conducted at the request of PIU in September last year. Almost 60% of respondents indicated that they want to receive medical packages from their employers and are ready to participate in their funding. In the case of 64% of respondents who already have private health care, its cost is at least partially covered by the company. This is not the case for small companies in which workers cannot count on co-financing of healthcare as part of supplementary insurance by employers. According to the ‘Small business research report regarding charges linked to the Social Insurance Institution’, prepared by the INDICATOR Marketing Research Centre, 68% of small business owners do not offer their employees additional health insurance. For 34% of the respondents, the cost is too high, taking into account the high financial burden of compulsory Social Insurance Institution contributions and taxes.

More information about healthcare can be found in PIU report: ‘Financing healthcare for employees’.

In 2018, the sum of insured turnover of Polish companies exceeded, for the first time in history, PLN 0.5 trillion and was 10% higher than in the previous year. The total amount of insured receivables is approx. PLN 157 billion, i.e. 9% more than in 2017.

According to data from the Polish Chamber of Insurance, the involvement of Polish insurers in supporting exports has increased considerably. The growth rate in the coverage of export loans amounted to 112%. Last year, Polish companies increased their exports considerably, resulting in demand for this type of insurance. However, the value of insured domestic receivables decreased from PLN 105 billion to PLN 101.7 billion. The reason for the decrease is the deteriorating financial situation of companies, despite high GDP growth last year. Many companies are unable to compensate for increased business costs with higher prices. In January this year, 98 companies were insolvent, which represents an increase of 20% YoY. In February this year, 47 bankruptcies were declared. ‘Payment backlogs are increasing, which is reflected in the risk management policy in insurance companies’, said Rafał Mańkowski, expert analyst at PIU.

Although the value of compensation payments decreased in 2018 (by 8%), some insurance companies established higher provisions for future payments. ‘The financial standing of businesses is deteriorating and this may result in higher compensation payments in 2019’, explained Rafal Mańkowski.

Trade credit is a more important source of short-term financing for businesses than short-term bank loans. This is also visible in the insurance sector. The national exposure of receivables insurance at the end of December last year was higher than the total amount of short-term loans granted by banks.

| Amount (PLN million) | 2017 | 2018 | YoY dynamics (%) |

| Domestic exposure (as at 31 December) | 105 168 | 101 729 | 97 |

| Export exposure (31 December) | 49 254 | 55 208 | 112 |

| Total exposure (31 December) | 154 422 | 156 937 | 109 |

| Insured domestic turnover | 358 953 | 399 512 | 111 |

| Insured export turnover | 98 139 | 105 389 | 107 |

| Total insured turnover | 457 092 | 504 901 | 110 |

| Gross premiums written | 550 | 612 | 111 |

| Gross compensation and benefits paid | 407 | 374 | 92 |

You are invited to read the report from the Polish Chamber of Insurance, describing the bancassurance market in Poland in 2018. The premium obtained in the bancassurance channel amounted to PLN 5.7 billion in Chapter 1 and 1.95 billion in Chapter 2.